We Spent $3.3M Buying Out Investors: Why and How We Did It

CEO and co-founder @ Buffer

Last month, Buffer spent $3.3 million – about half of all the cash we had in the bank – to buy out our main venture capital (VC) investors.

Starting the conversations, negotiations, and process of this buy out was one of the most important decisions I’ve made in the Buffer journey so far, and it was the culmination of more than a year of work. This is a key inflection point for Buffer that puts us truly on a path of sustainable, long-term growth.

Here is the full journey of how we decided on this path for the company, including all the details and numbers involved in carrying out a stock buyback of seven of our sixteen Series A investors.

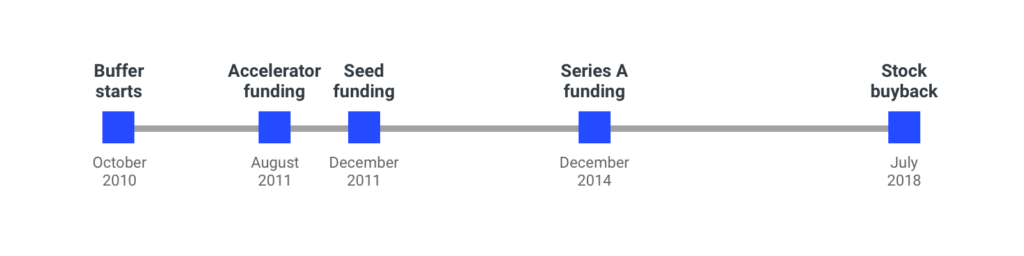

Buffer’s funding history

Here is a summary of funding raised for Buffer since we started in 2010:

- October 2010: Buffer was born and initially bootstrapped through revenues

- August 2011: Buffer was accepted into AngelPad startup accelerator, with initial $120,000 investment

- December 2011: Buffer raised a small seed round of $330,000, to bring total funding to $450,000

- December 2014: Buffer raised Series A of $3.5 million, to bring total funding to $3.95 million

- July 2018: Buffer bought out main Series A investors (investors representing $2.3 million of the $3.5 million raised)

In general, we’ve taken the approach of being profitable and having decent revenue at the time of raising funds. As a result, we’ve been able to raise funding on good terms and keep a fair amount of control. Following each round, we eventually dipped into negative cashflow as a result of accelerated hiring but always had a manageable plan to get us back to profitability.

Finding and working with a non-traditional VC

Back in 2014 when we raised our Series A, my co-founder and I had the objective to put together an atypical round. As mentioned in our funding announcement, there were several things that made our Series A different from a traditional startup Series A:

- Raising a relatively small amount ($3.5 million in funding when doing $4.6 million in annual revenue)

- Not giving up the usual 20–30 percent of the company (we raised $3.5 million at a $60 million valuation, giving up 6.2 percent)

- Not giving up control (no investor board seat)

- Taking liquidity to de-risk and go long ($2.5m of $3.5m was for founders and early team)

- Not being boxed in to an IPO five to seven years from raising funding

In our search for a unique investor happy with our conditions, we found Collaborative Fund, and they agreed to lead our Series A funding by putting in 60 percent of the funds. With them as our lead, we found other investors who also approached things differently and we were very proud of the outcome.

At the time of the Series A, we felt on top of the world. We had around $4.6 million in ARR (annual recurring revenue) and were growing revenues around 150 percent per year. We were at a point where we felt like we could “have it all,” and in many ways we did: we got the VC funding at the ideal terms, we kept control, we took some liquidity, and we continued to operate with full transparency and as a fully remote team. Based on our growth rate, we didn’t foresee any problem in giving a great return to Series A investors and were very excited to make a few bigger bets to see where we could take Buffer.

Although our goal was to see that growth trend continue, we shared openly that we may not want to raise further funding, sell the company, or IPO. We were transparent that we wanted to be able to keep questioning the way things are done. Specifically, we communicated that we wanted the option to be able to give a return via distributions, not an exit.

Collaborative Fund suggested that we account for these various paths within the structure of the Series A funding. We added downside protection for the Series A investors, in the form of a right to claim a return of 9 percent annual interest on their investment at any point starting five years after the initial investment. At the time, I didn’t appreciate how important this clause would become. Even our legal counsel commented that this was not something he saw too often.

The evolution of Buffer and our fit with VC funding

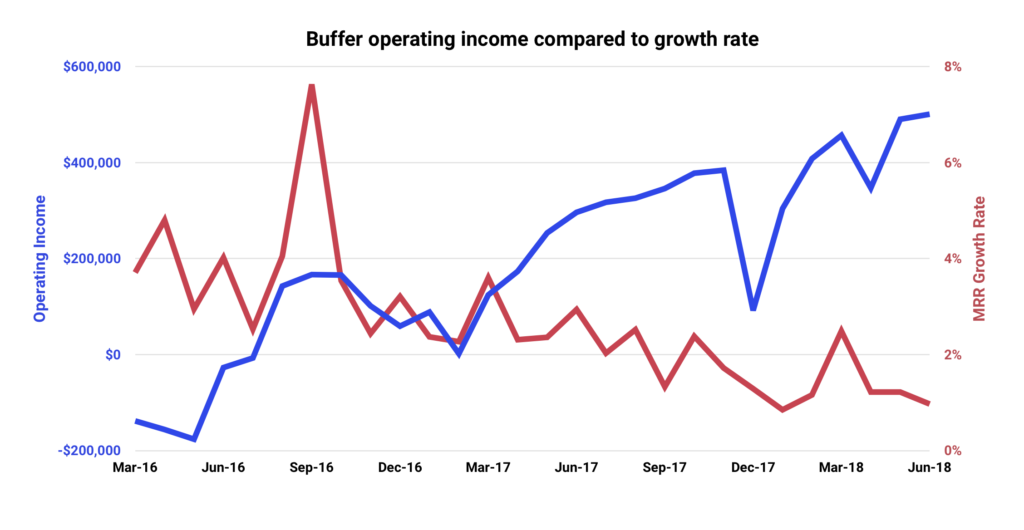

Buffer has had an interesting and somewhat rocky few years since that Series A funding. In mid–2015, in an effort to keep our growth rates high and comparable to startups with much more funding, we grew the team rapidly and tried to increase our pace of product development. We found ourselves with financial struggles after growing expenses without results following quickly enough. The rate at which our bank balance was decreasing made us realize that we didn’t have a proper grasp of our financials. Our financial situation presented a key turning point for us: Would we solve this by raising more funding or by cutting expenditures? In one of my most excruciating decisions, we chose to solve the situation without outside funds and did a round of layoffs to become profitable.

After making these tough decisions and changing some fundamental internal operations, we became profitable within a few months. While profitability was exciting, our growth rate suffered. Within the leadership team we started to discuss what growth rate we wanted to achieve. Whereas in the past we’d “had it all” and achieved growth alongside creating a unique culture with a fully remote team and high levels of transparency, it now started to feel like we had to choose between those things. It was suggested that some of the fundamentals that I had come to value could be removed to create a productivity environment that would increase the growth rate. I refused to compromise on the transparency and remote work aspects of our culture, so we started to explore slower growth goals, and what that would mean for the future of Buffer. Ultimately, my co-founder Leo and our CTO Sunil left the company in early 2017 based around this foundational vision decision.

As a result of the tumultuous events of layoffs, leadership misalignment and eventual departures, I was noticing a breakdown in some of our core values and what made us special and different. To me, these were fundamental values that shape not only how Buffer feels, but also how we perform. I decided to dig in, make some changes and grow back the trust of the team.

Those adjustments were not easy. Alongside growing our profitability and becoming sustainable for the long-term, I also had to figure out how my role would be different without my co-founder, and how to effectively manage the leadership team alone. It has been completely worth it, because we accomplished this all while staying true to our core values and unique ways of working. We opted for calm company growth that allows team members to bond and have time to become productive, rather than having a large portion of the team be completely new to Buffer. We became very profitable and started to work on longer-term projects to diversify our product offerings and revenue sources. This was in contrast to the more traditional venture-backed startup path of having a burn rate and relying on continual rounds of funding with the goal to maximize growth rate above all else. We could have hired outside senior leadership, grown the team considerably and pushed for hyper growth, but I believed that it was not the best path for Buffer.

As the months passed and we made progress towards long-term sustainability, our net profit margin grew from months of losses to 7 percent to consistently exceeding 25 percent. We started to have months where we had profit of $300,000 to $500,000 and the bank balance started to grow rapidly. The challenge with this, though, was that our growth rate had decreased. This was a trade-off I was willing to make. Naturally, the decreased growth rate, combined with my co-founder leaving, began some challenging conversations with Collaborative Fund. Buffer was not on a traditional venture-funded path anymore, and I have full empathy for how this made us less interesting in the eyes of our lead investor.

In the first half of 2017 I had a number of conversations with Collaborative Fund. They were around two years into their investment, and given Buffer’s refocused path of sustainable growth, the topic of the previously mentioned 9 percent return downside protection naturally arose. The downside protection offered a time-frame and guarantee of returns. While discussing this further, I was taken aback when I was asked whether I would step down as CEO in the event that Buffer could not afford the 9 percent annual return. Although it may be a reasonable question from a pure business perspective, and I was confident we’d be able to deliver, it shocked me to my core. The level of communication we once had started to break down after that and it triggered much reflection and some sleepless nights for me.

Why we chose to buy out our main VC investors

By late 2017, it was clear that Buffer had become less of a fit for VC funding. Month by month we increased our financial sustainability by growing our profit margin. We also worked hard to create and promote a culture where team members could enjoy their work for years without leading to burnout.

With healthy profits leading to our bank balance growing from $2 million to over $5 million, we could see that we were on a path towards being able to afford the 9 percent downside protection return for our Series A investors. By this point, our seed investors had been supporting the company for almost six years, and several were starting to ask when they may get a return.

The Series A class of shares included a protective provision which meant that Buffer was unable to offer liquidity for other shareholders (seed or common) without approval from a majority of the Series A. In order to get Buffer into a situation where we could more freely offer liquidity to early investors and team members, we knew that the first step would be to buy out the Series A investors and adjust this protective provision.

By moving ahead with a stock buyback for our Series A investors, we would be able to unlock this ability to give other shareholders a return, and we would put the company squarely on a path of long-term sustainability. I believe that the market is still wide open for Buffer to continue to grow, and I’ve fallen in love with the way we work and the incredible team and customers I get to work with. I began to pursue buying out our VC investors in earnest.

How we prepared for and carried out a stock buyback

The first key step in working towards buying out our main VC investors was to build up the cash reserves to make it possible. One way we did this was to ensure that our revenue growth rate exceeded our rate of hiring. Next, I reached back out to Collaborative Fund, and a couple of other key investors in our Series A, about the downside protection. I initiated the discussions and then handed this over to our Director of Finance, Caryn Hubbard.

Caryn did a great job of having productive conversations with investors and gradually converging with them on a deal that everyone could agree to. Our finalized terms were very close to the pre-determined 9 percent return included in the Series A terms. We moved the date forward and proposed that we could offer this return three-and-a-half years into their investment rather than after five years.

As part of the transaction, we also amended the protective provisions of the Series A shares to allow Buffer to have the ability in the future to offer liquidity to seed investors and common shareholders (mostly early team members). In order to achieve this, there were specific thresholds of approval we needed from each set of shareholders:

- Approval from 60 percent of Series A shareholders

- Approval from 50 percent of Preferred shareholders (combination of Series A and Seed investors)

- Approval from 50 percent of All shareholders (including Common)

This took some delicate communication and investor relations work, which Caryn and I worked on together. Overall, it was straightforward to achieve these approvals once we explained our reasons for moving ahead with this stock buyback and the possibilities it would open up for the future. As I personally own over 45 percent of stock, meeting the final threshold of approval was simple once we had our investors on board.

Caryn worked closely with our legal counsel to put together the documents for these approvals, and to ensure we had considered every angle. The stock buyback was set up as a tender offer and followed specific tender offer rules. A key concept is that every shareholder receives the same information in order to make their decision on whether to sell shares.

With that, we started the stock buyback process. We gave every Series A shareholder the option to sell their shares at the agreed return. The resulting valuation was $80.8 million, representing a 40.5 percent return over three-and-a-half years.

All investors had a twenty-day period to make their decision on whether to sell, as part of the tender offer. Once we had all the responses back from investors, we processed the transactions (our biggest ever wire transfers!) and our legal counsel completed the transaction by transferring the stock certificates.

The impact of buying out Series A investors

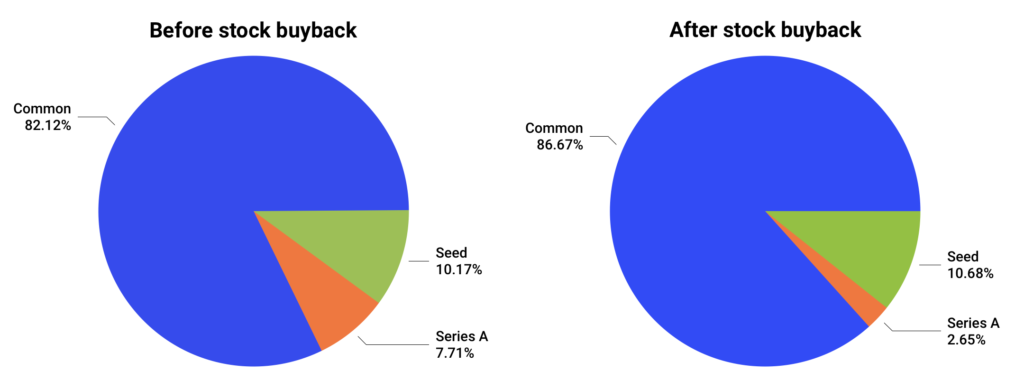

Our two main VCs made up 60 percent of Series A shares. Beyond that, five more investors chose to sell their shares for a total of 67.29 percent of Series A shares bought back by the company.

Now that the stock buyback is complete, the ownership of Buffer has changed somewhat. The Series A investors now hold 2.65 percent of outstanding shares, and those with Common or Seed shares saw an ownership increase of ~5 percent.

Note: these charts don’t include our employee stock option pool. All team members at Buffer have stock options and, as they are exercised, other outstanding shares are diluted. Currently, a further 10 percent of Buffer is allocated to stock options.

The impact of the buyback on our bank balance was $3.3 million. Our balance after the transaction remained healthy at over $4 million. Our net profit has continued to be around $400,000 to $500,000 per month and we have already surpassed $5 million in the bank. If you’d like to follow along with our quarterly transparency reports with more of our financial information, they are available here.

Thanks for reading

We have been very happy to give investors a return and also create better alignment within our shareholder base towards the path we are on. I’m grateful that many Series A investors, especially angel investors from the seed round, chose to stay on board for the journey ahead. We will be considering stock buyback opportunities in the future, as well as alternative sources of funds, in order to provide liquidity for other investors and team members.

I’m confident that the small business market is still wide open for Buffer to continue to grow, and I’m committed to continuing to build great products our customers love and cultivate a workplace culture of trust, freedom and flexibility. These are the things that drive me and form my deeper personal purpose. This stock buyback is another step in the right direction that signifies to me that this will be a very long-term endeavor. Now, more clearly than ever, we have the privilege to continue thanks to the revenues from our paying customers.

I truly believe that we should be talking more about these topics as an industry, and I hope our experience can be useful to those who may be considering a similar path. I invite you to leave a comment on this post and share your thoughts on the topic.

Try Buffer for free

140,000+ small businesses like yours use Buffer to build their brand on social media every month

Get started nowRelated Articles

TikTok's parent company must divest the app or face a ban in the U.S. Here's everything we know, plus how to plan ahead.

How the Buffer Customer Advocacy Team set up their book club, plus their key takeaways from their first read: Unreasonable Hospitality by Will Guidara.

In this article, the Buffer Content team shares exactly how and where we use AI in our work.